Change Ripples from D.C. and Beacon Hill

By Christopher R. Vaccaro

Special to Banker & Tradesman

The Greek philosopher Heraclitus stated centuries ago that change is the only constant in life. A few things expected to bring change to the Massachusetts real estate industry in 2025 are discussed below.

The MBTA Communities Act

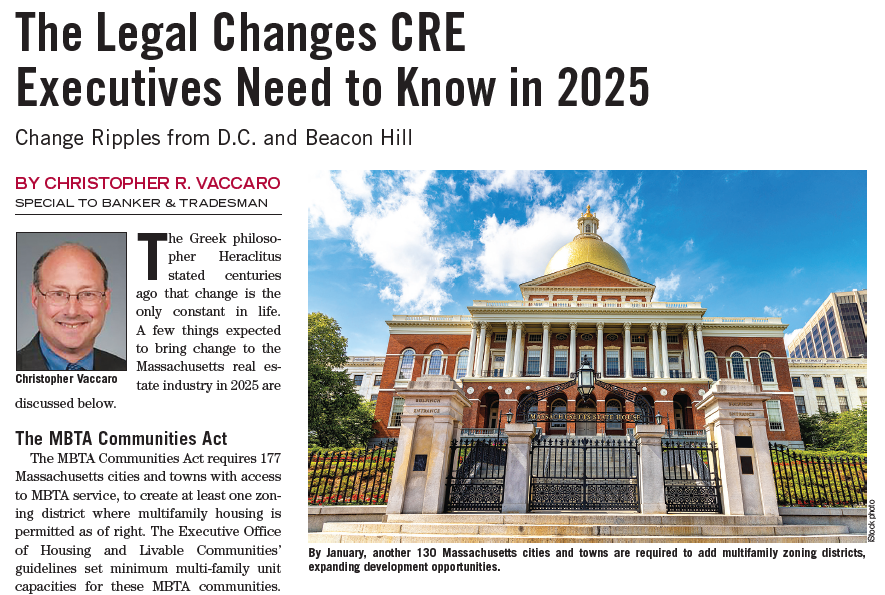

The MBTA Communities Act requires 177 Massachusetts cities and towns with access to MBTA service, to create at least one zoning district where multifamily housing is permitted as of right. The Executive Office of Housing and Livable Communities’ guidelines set minimum multi-family unit capacities for these MBTA communities. EOHLC issues determinations of compliance to communities that meet its guidelines.

Most MBTA communities have achieved full or interim compliance with EOHLC guidelines, but not the town of Milton. The guidelines require Milton to establish a 50- acre zoning district accommodating at least 2,461 multi-family housing units. Milton’s town government tried to comply, but local opposition thwarted its efforts. The opposition organized a referendum, and Milton’s voters rejected the zoning change.

Attorney General Andrea Campbell promptly sued Milton in the Supreme Judicial Court, seeking an injunction requiring Milton to adopt a compliant zoning amendment.

The attorney general’s suit relies on provisions of the Zoning Act that give courts jurisdiction to enjoin zoning violations. Courts typically use this power against property owners who disregard zoning limitations on building dimensions or uses. The attorney general’s lawsuit to force a municipality to adopt a specific zoning bylaw is an unusual use of the Zoning Act.

The SJC heard arguments on this case in October. It is expected to issue a decision early next year. The real estate community and housing advocacy groups are standing by.

The Affordable Homes Act, enacted last August, includes numerous spending and housing production policies, many of which will take years to deliver results. But one component of the AHA is likely to have a meaningful impact soon.

Affordable Homes Act

The AHA requires that local zoning laws allow at least one accessory dwelling unit (ADU) as-of-right in single-family zoning districts throughout Massachusetts (but not in Boston).

Municipalities cannot require owner occupancy of either ADUs or principal dwellings. The size of an ADU is limited to the lesser of one-half the gross floor area of the principal dwelling or 900 square feet. Reasonable regulations for site plan review, building dimensions and short-term rentals are allowed.

This simple zoning law change has excellent potential to add badly needed dwelling units in Massachusetts.

Offshore Wind Turbine Projects

Massachusetts is expected to be a major staging area for offshore wind turbine projects in federal waters south of Martha’s Vineyards. Vineyard Wind is already under construction, promising to generate clean energy for over 400,000 homes and businesses.

However, Avangrid’s Commonwealth Wind project stalled. That project was expected to generate enough clean energy for over 700,000 homes.

Avangrid originally entered into long-term power purchase agreements (PPAs) with several utility companies at set prices. Later, it sought to undo the PPAs, claiming that the project was now uneconomic because of inflation, higher interest rates, supply chain problems and other disruptions.

The Department of Public Utilities approved the PPAs over Avangrid’s objections, whereupon Avangrid withdrew from the project.

Another clean energy firm may build this project, but President-elect Donald Trump is no proponent of offshore wind turbines, which depend on leases and other financial incentives from the federal government. The growth of this industry in Massachusetts is at risk.

The End of Chevron Deference

Chevron deference is a legal doctrine that gave federal agencies broad latitude to interpret enabling legislation and promulgate regulations.

The U.S. Supreme Court formulated this doctrine four decades ago in Chevron U.S.A., Inc. v. Natural Resources Defense Council, Inc. In that case, the EPA issued new air pollution regulations that eased permit requirements for polluting industries that modify their plants.

The Supreme Court ruled against an environmental watchdog group that challenged the EPA, holding that when Congress implicitly delegates authority to an agency, courts cannot substitute their own construction of the enabling legislation for the reasonable interpretation of the agency’s administrator.

Last June, the Supreme Court overruled Chevron in Loper Bright Enterprises v. Raimondo. Owners of fishing vessels had challenged a National Marine Fisheries Service’s regulation requiring the fishing industry to pay for on-board observers enforcing the service’s fishery management plan.

Courts now must exercise independent judgment in deciding whether an agency acted within its statutory authority. They cannot readily defer to agency interpretations of ambiguous statutes.

Loper gives federal courts more scrutiny over federal agencies’ actions, which is expected to increase litigation involving those actions.

Download the article as seen in Banker & Tradesman on October 28th, 2024. Learn more about Christopher R. Vaccaro.